Trading session overview

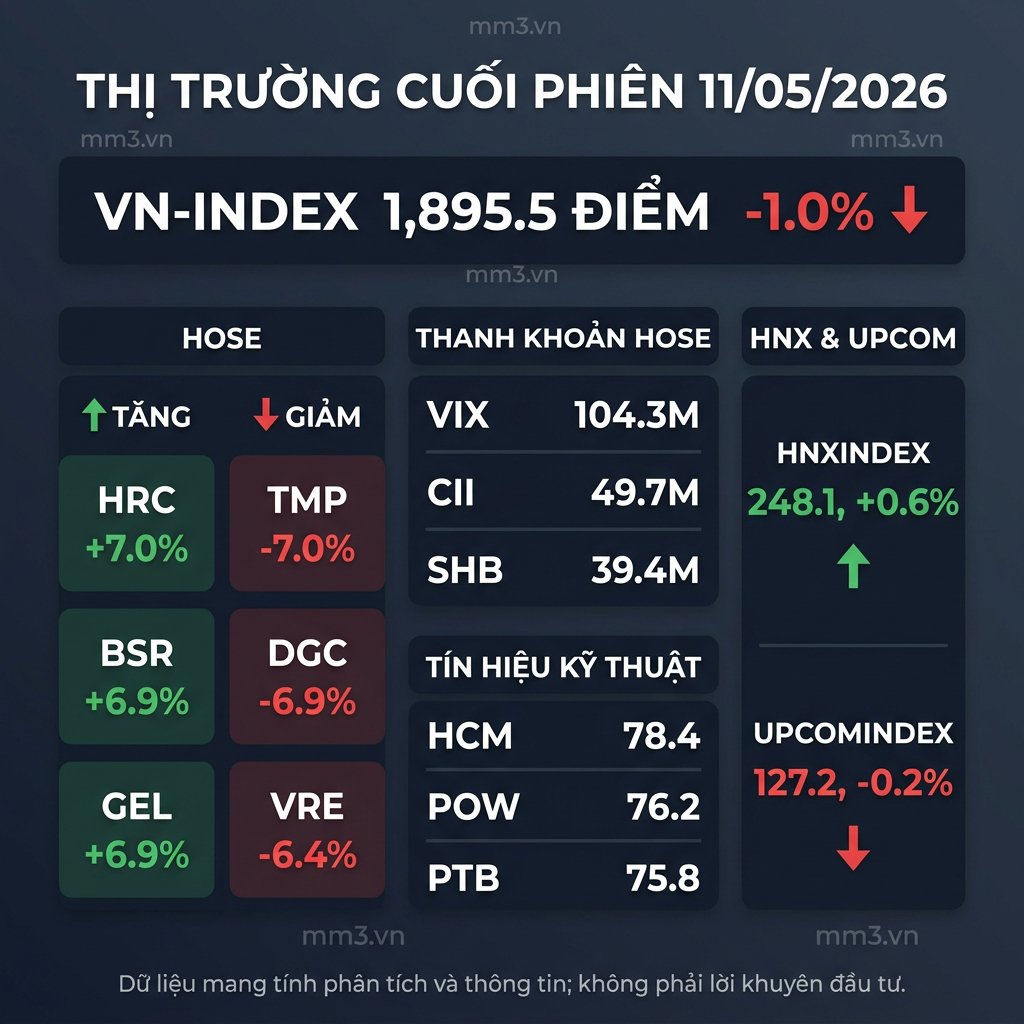

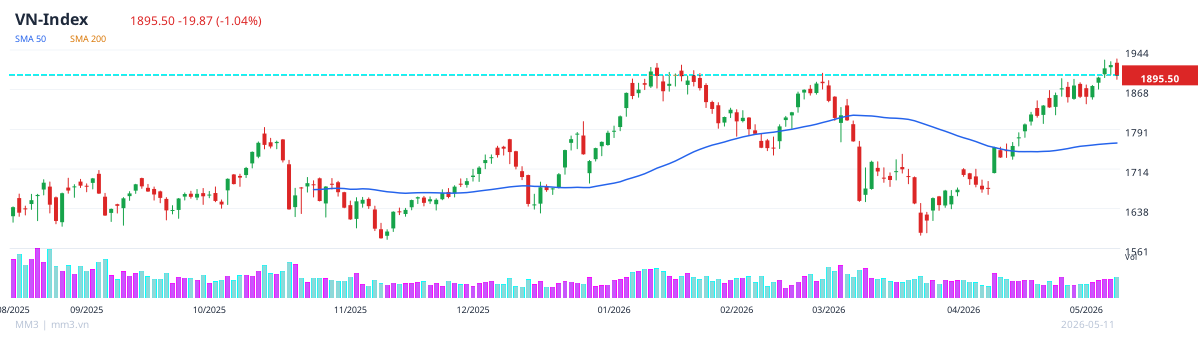

The market at the end of the 11/05 session recorded clear differentiation across the three exchanges. VN-Index closed at 1,895.5 points, down 1.0%, while market liquidity remained high with a total order matching volume of nearly 960.7 million shares on HOSE. The market breadth leaned towards correction as large-cap stocks faced pressure, although some individual stocks maintained positive technical structures.

On the index movement side, HNX-Index increased by 0.6% to 248.1 points, while UPCOM-Index decreased slightly by 0.2% to 127.2 points. This differentiation indicates that cash flow tends to rotate to the mid-cap and small-cap groups, while profit-taking pressure continues to weigh on leading stocks on HOSE.

Prominent stock groups

On HOSE, the strongest growing stocks of the session were HRC (+7.0%), BSR (+6.9%), and GEL (+6.9%). These were rare bright spots in a market dominated by correctional pressure across many key sectors.

Conversely, TMP (-7.0%), DGC (-6.9%), and VRE (-6.4%) were among the biggest decliners. This movement reflects significant volatility in stocks attracting cash flow attention but lacking broad market consensus.

Liquidity and market breadth

Liquidity was the most notable point in the session as many stocks traded actively. Leading in order matching on HOSE was VIX with 104.3 million shares, followed by CII with 49.7 million shares and SHB with 39.4 million shares.

The large trading volume in these stocks indicates that cash flow is still present but is highly dispersed according to individual stories rather than spreading evenly across the market. Therefore, market breadth leaned towards selective trading, with only a few stocks maintaining a clear upward trend.

Sector analysis

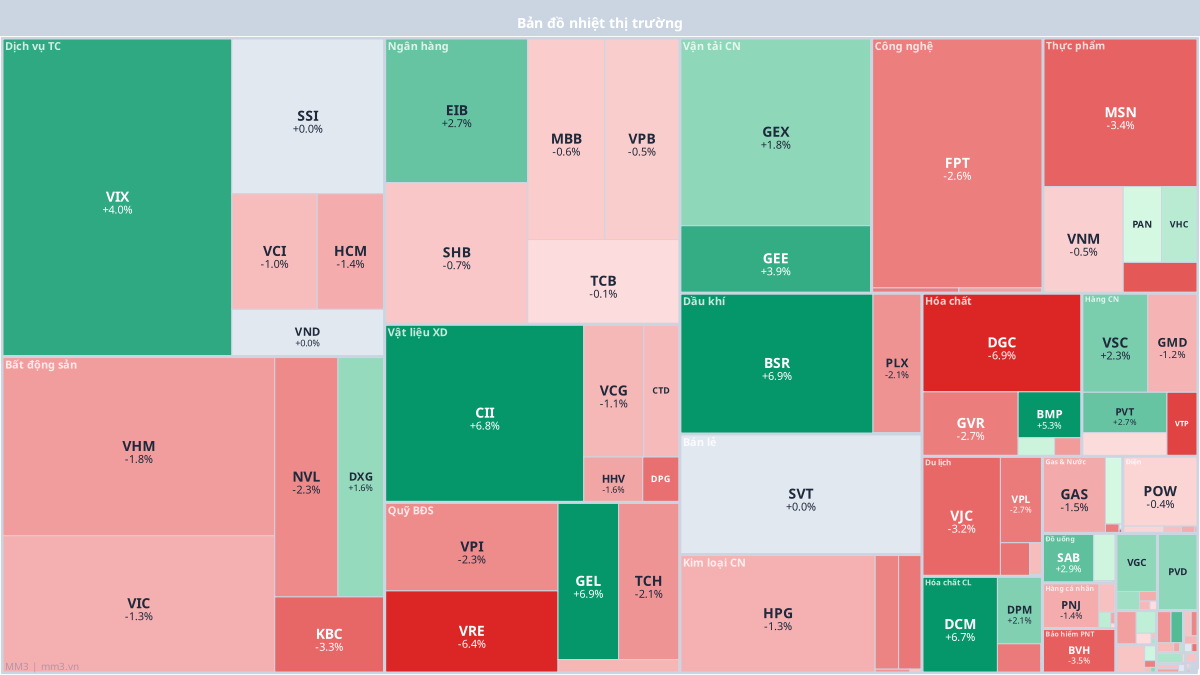

From a sector perspective, finance and construction materials continued to be the focus of liquidity, but price movements were inconsistent. Notably, VIX stock increased by 4.0% with a trading value of over 2,018.0 billion VND, while CII increased by 6.8% and BSR increased by 6.9%, showing that cash flow is still willing to chase some stocks with specific narratives.

Conversely, many stocks in the technology, chemical, retail, and real estate sectors faced significant pressure. FPT decreased by 2.6%, DGC decreased by 6.9%, VRE decreased by 6.4%, indicating that differentiation pressure is creating a large gap between sectors within the same session.

| Sector/Industry | Notable Movement | Observation |

|---|---|---|

| Financial Services | VIX, SSI, VCI, HCM, VND | Strong cash flow concentration, but high differentiation |

| Real Estate | VHM, VIC, NVL, DXG, KBC, VRE | Many stocks facing correctional pressure |

| Chemicals | DGC, GVR, BMP, DPR, PHR | Strong fluctuations, wide price ranges |

| Oil and Gas | BSR, PLX, TDG | Individual bright spots emerged |

Notable technical signals

Among stocks with positive technical signals, HCM achieved a composite score of 78.4 with an RSI of 59, and MACD and EMA in positive territory. Following were POW with 76.2 points, and PTB with 75.8 points, indicating that some stocks maintained stable price bases and trend structures compared to the general market.

These signals reflect the potential for technical recovery in individual stocks, especially as cash flow has not completely withdrawn but is rotating. However, the general index decline amid high market breadth suggests that short-term volatility risks remain significant.

Outlook for the next session

Technically, the VN-Index is approaching the short-term resistance zone around 1,900 points, while the nearest support zone is being monitored around 1,880-1,885 points. If demand is not strong enough to absorb profit-taking pressure at higher levels, sideways trading may continue in the following sessions.

Investors should pay attention to the reaction of large-cap stocks, especially those leading liquidity such as VIX, CII, SHB, and stocks with good technical signals like HCM, POW, PTB. Additionally, international developments and domestic cash flow will continue to be two decisive factors for the market's short-term status.

For analysis and information reference only, not investment advice.